- Key Insights

- Halifax Robert L Stanfield International Airport Trends

- Regional Analysis of Tourism Accommodation Trends Across Nova Scotia

- Trends in Hotel Stays and Room Share in Halifax

- Place of Origin of First-Time Visitors to Nova Scotia

- Costs and Consequences of Weak Tourism Policies in Halifax

- Interventions and Solutions to Weak Tourism Policies

- The Future of Tourism in Halifax

- References

Key Insights

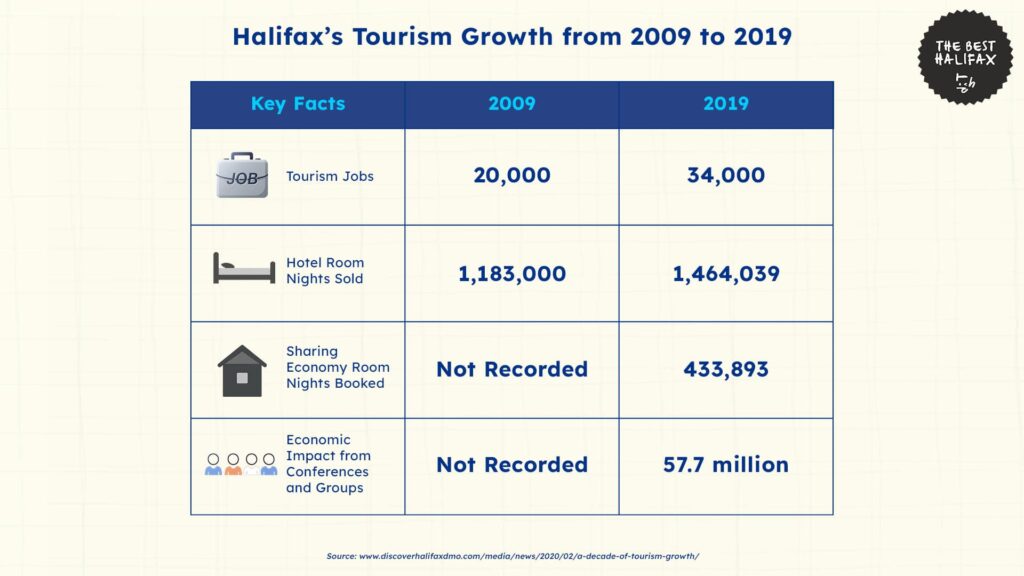

| According to Discover Halifax, the city’s tourism sector supported approximately 20,000 jobs in 2009. This figure then rose by 70% to 34,000 by 2019. Data from Tourism Nova Scotia indicates that in 2023, fixed-roof accommodations across the province reached an average occupancy rate of 66%, with 282,000 room nights sold. The same report shows that Halifax Metro recorded the highest accommodation activity in 2023, with a 75% occupancy rate and 146,000 room nights sold. Findings from the Nova Scotia Exit Survey show that the highest share of first-time visitors to the province come from international markets, with 64% of travelers coming from the northeastern region of the United States. The Tourism Industry Association of Canada reveals that one of the primary barriers to growth in Canadian tourism is a lack of tax competitiveness, as the country remains one of the few that does not zero-rate its tourism services. |

Discover Halifax gives an overview of the state of tourism in Halifax over the past few years.

Their report shows that employment is the strongest indicator of tourism growth in the city, as the tourism industry generated around 20,000 jobs in 2009. By 2019, this number jumped to 34,000, which is an increase of 70% over 10 years.

This shows how significant tourism has become in the creation of jobs, particularly in areas like hospitality, transportation, entertainment, and travel services.

The demand for accommodations has grown as well. Between 2009 and 2019, the total number of hotel room nights sold grew from 1,183,000 to 1,464,039.

This growth of 24% implies that there has been an increase in visitors to the city and a greater occupancy rate year-round. This also shows that Halifax enhanced its reputation as a seasonal destination, both for leisure and business travelers.

In addition to hotels, alternative kinds of accommodation have also started emerging. The sharing economy, which had no recorded presence in 2009, accounted for 433,894 room nights by 2019.

This increase in alternate lodging facilities reflects the changes in travelers’ behavior as well as the influence of internet platforms such as Airbnb.

Meanwhile, tourism expansion also provided stronger economic benefits. In 2019, group travel and conferences amounted to 57.7 million dollars in direct expenditure.

This amount further illustrates how Halifax not only brings in independent tourists but has also become a potential destination for business meetings, conventions, and organized group tourism.

Together, all of these trends show how Halifax has evolved throughout the decade into a vibrant and diverse tourist destination.

Halifax Robert L Stanfield International Airport Trends

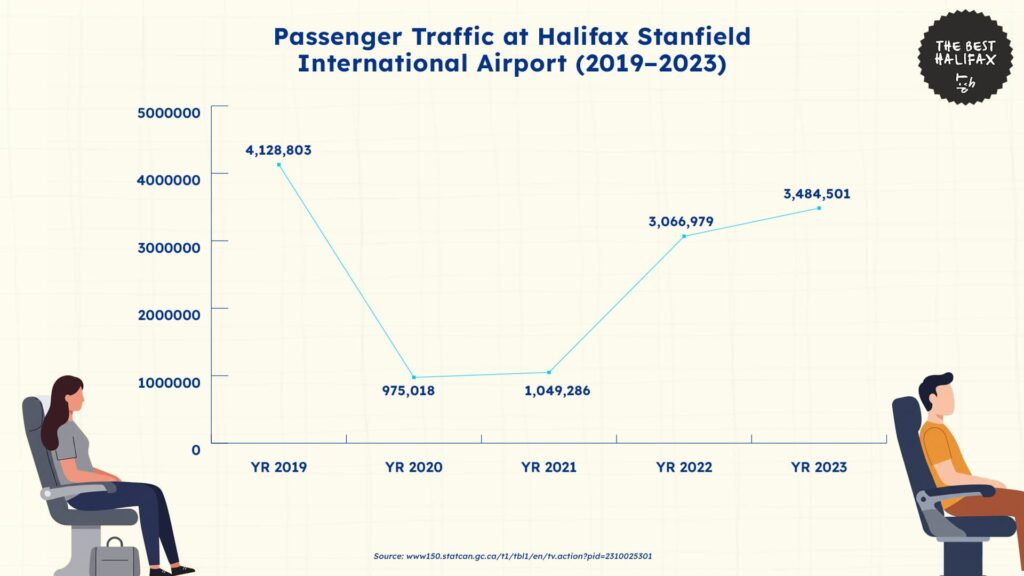

Data from Statistics Canada reveals the state of passenger traffic in the Halifax Robert L. Stanfield International Airport from 2019 to 2023.

In 2019, the airport handled 4,128,803 total passengers, both enplaned and deplaned. This figure was recorded during a fully operational year with strong domestic and international activity, which played a significant role in the flow of tourists arriving.

However, in 2020, total passenger traffic fell to 975,018. This is a 76% decrease from the year before and shows the effects of the pandemic on travel and tourism in Halifax.

This sharp fall highlights the effects of national and international travel bans, suspensions of airline routes, and public health policies that weakened travel demand.

The next year, 2021, saw just a limited recovery. Passenger traffic was up to 1,049,286, which is a slight 8% increase from 2020 but is still 75% short of pre-pandemic levels.

These statistics illustrate that air transportation to and from Halifax continued to be severely restricted despite the gradual loosening of travel bans and restrictions.

The airport did not experience significant recovery until 2022. Total passengers rose to 3,066,979 due to the return of commercial routes, growing consumer confidence, and the relaxation of most entry restrictions.

This recovery was a 192% increase from 2021 levels and showed that there was renewed demand for both leisure and business travel.

In 2023, the airport served 3,484,501 passengers, which is up 14% from 2022. Although the figure is still 644,000 passengers short of the rate in 2019, the steady growth for two years in a row shows that Halifax is slowly regaining its pre-pandemic numbers.

If this trend continues, passenger numbers might reach or surpass pre-pandemic levels by 2025, especially as route expansions are pursued and international market access is enhanced.

This increase in passenger traffic is tied to more general tourism activity in Halifax.

With more visitors coming by air, particularly from long-haul markets such as the United States and Western Canada, demand for accommodations, transportation, and visitor services continues to increase.

Ensuring that airport infrastructure keeps up with increasing travel volume will be critical to maintaining tourism-driven economic benefits in the area.

Regional Analysis of Tourism Accommodation Trends Across Nova Scotia

Tourism Nova Scotia gives insights into the overall state of tourism in the province, particularly when looking at accommodation trends.

The data shows that in 2023, tourism was relatively stable, with only some increases and decreases across cities.

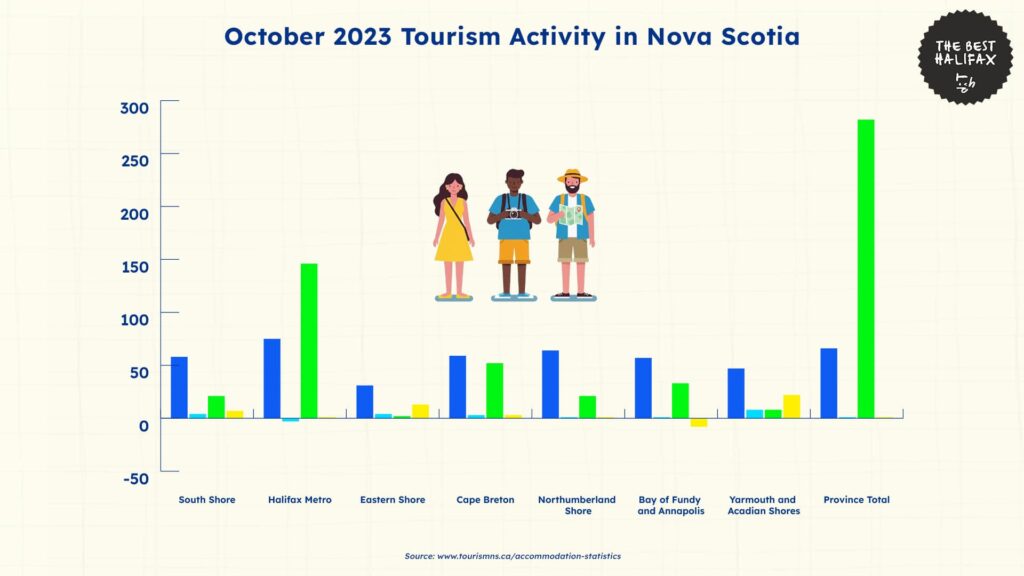

When looking at the province’s average for October 2023, fixed-roof accommodations achieved an average occupancy rate of 66%, with 282,000 room nights sold.

Compared to the previous year’s number, this shows a 1 percentage point increase in occupancy and a 1% increase in bookings.

Halifax Metro has the highest number of tourists accommodated. The city was at 75% occupancy and sold 146,000 room nights, which was more than any other region within the province.

Despite these high figures, occupancy in Halifax dropped by 3 points and had no growth in bookings overall.

Conversely, the South Shore experienced a slight increase. Their occupancy was at 58%, which is a 4-percentage-point rise from the previous year. Room nights sold also reached 21,000 – another increase of 7% compared to October 2022.

This type of growth indicates that travelers are spending more time in this coastal area during the fall.

Similarly, Cape Breton experienced 59% occupancy and 52,000 room nights sold. Both occupancy and bookings were 3% higher, which shows steady interest and ongoing travel for the city.

Northumberland Shore also receives a high number of tourists. It had 64% occupancy and 21,000 room nights sold, which are both 1% higher than last year and indicate that the area has a solid source of visitors.

The Eastern Shore, though still the least busy area overall, experienced the largest growth rate in bookings. Their occupancy was 31%, an increase of 4 points, and room nights sold were up 13% to 2,000.

While this lower volume indicates that it is still a smaller contributor to provincial tourism, its high growth indicates good momentum for the area.

Meanwhile, the Fundy Bay and Annapolis Valley registered more uneven numbers. Occupancy increased by 1 point to 57%, while bookings dropped by 8%, with 33,000 room nights sold.

This decline indicates fewer visitors in total or shorter stays, which could be caused by changes in business activities or fewer fall-specific travel attractions.

However, Yarmouth and the Acadian Shores saw the greatest decrease. While occupancy increased by 2 points to 47%, room nights sold dropped to 8,000 – a 22% decrease from October of the previous year.

This difference between increased occupancy and decreased volume could indicate fewer rooms or less demand in general.

Overall, these statistics point to a stable tourism landscape in Nova Scotia, with Halifax leading the province’s growth.

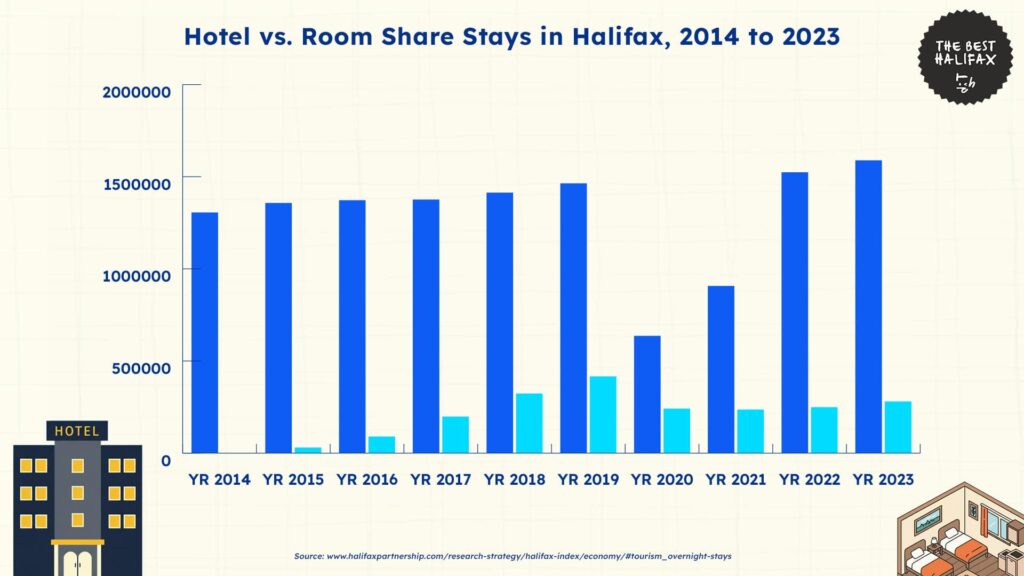

The Halifax Partnership shows how, in the past decade, there has been a clear shift in where visitors to Halifax are choosing to stay. While hotel accommodations remain dominant, room-sharing stays have also grown significantly.

Between 2014 and 2019, hotel overnight stays increased consistently. Hotel bookings went up from 1,305,960 in 2014 to 1,464,039 in 2019, representing a 12% rise over five years.

This increase illustrates the steady growth of tourism demand over the years, which was most likely supported by increased popularity, improved travel options, and continued marketing campaigns.

During the same period, room shares experienced even faster growth. Starting with 30,000 overnight stays in 2015, overall bookings climbed to 416,435 by 2019, which is a 1,288% rise over five years.

This illustrates the growing popularity of room-sharing platforms like Airbnb which offer flexible and generally cheaper substitutes for conventional hotels.

Room shares also accounted for 22% of all overnight stays by 2019, which is up 2% from 2015.

However, the pandemic impacted both industries in 2020. Hotel bookings fell by 57% to 636,408, while room share bookings fell by 42% to 241,468.

Although there was a smaller overall drop in room shares, the decrease in both industries shows the effect of pandemic travel bans and decreased visitor confidence during a health crisis.

The next year, both industries experienced some recovery. In 2021, hotel stays were up to 907,182, which is an increase of 42%.

This number continued to grow in 2022 and 2023, reaching 1,524,014 and 1,588,921, respectively.

Hotel stays by 2023 had also increased by 9% since 2019, which was a sign that the industry was not only back to normal but also surpassed its pre-pandemic levels.

Room shares, on the other hand, had not yet reached previous numbers. Following the drop to 236,652 in 2021, bookings recovered with only moderate increases to 249,276 in 2022 and 280,500 in 2023.

These numbers are 33% less than those of 2019. This indicates that though demand for alternative accommodations continues, it has not grown at the same rate as hotels after the pandemic.

This may have been caused by regulatory shifts, fewer listings, or changing consumer preferences.

Overall, the statistics indicate that Halifax’s overnight accommodation sector has stabilized despite having significant variations in recovery.

Place of Origin of First-Time Visitors to Nova Scotia

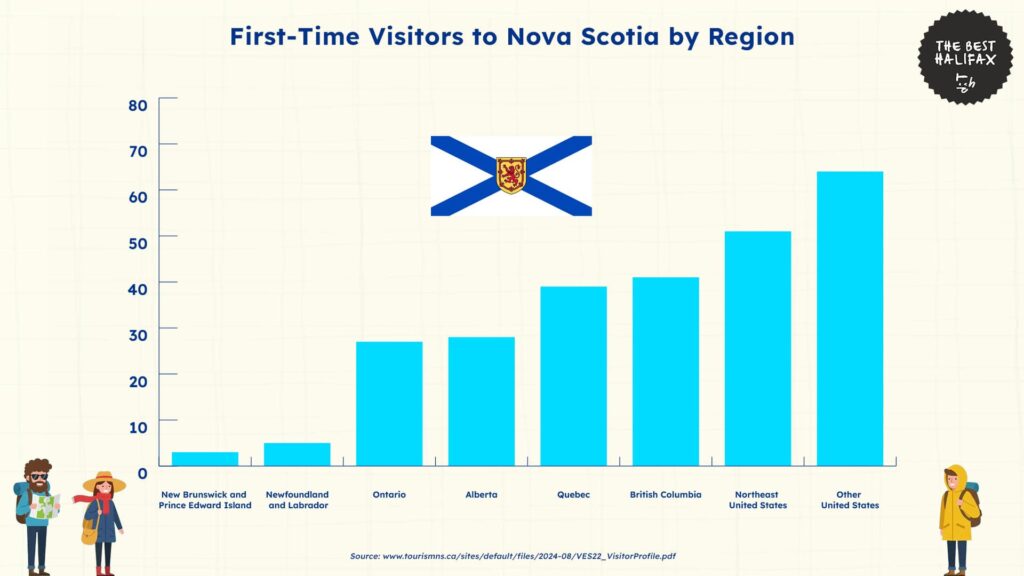

The Nova Scotia Visitor Exit Survey reveals where most tourists to the province are coming from.

In 2022, 23% of all overnight visitor parties to Nova Scotia were made up of first-time tourists. This is defined as those individuals who had never spent more than one night in the province before.

The groups that had the largest percentage of first-time visitors were from international destinations.

Visitors from outside of the northeastern area of the United States had the largest portion, with 64% of their population being first-time visitors to Nova Scotia.

Meanwhile, for travelers from the northeastern United States, 51% of their population were first-time visitors.

These figures show that United States travelers contribute greatly to first-time tourism within the province.

Within Canada, the top origin destinations for first-time visitors were British Columbia and Quebec. From these two destinations, 41% and 39% of visiting parties had never been to Nova Scotia before, respectively.

Alberta was third at 28%, and Ontario was fourth at 27%. These numbers show that there are opportunities to continue increasing visitation from provinces in central and western Canada.

Conversely, there were only a few Atlantic provincial visitors who were new to Nova Scotia. From New Brunswick and Prince Edward Island, there were only 3%, and Newfoundland and Labrador recorded 5%.

However, these percentages are also probably affected by the fact that these provinces are close to Nova Scotia, and many tourists have already visited in the past.

In general, the statistics indicate that Nova Scotia continues to attract new visitors from more distant locations.

Costs and Consequences of Weak Tourism Policies in Halifax

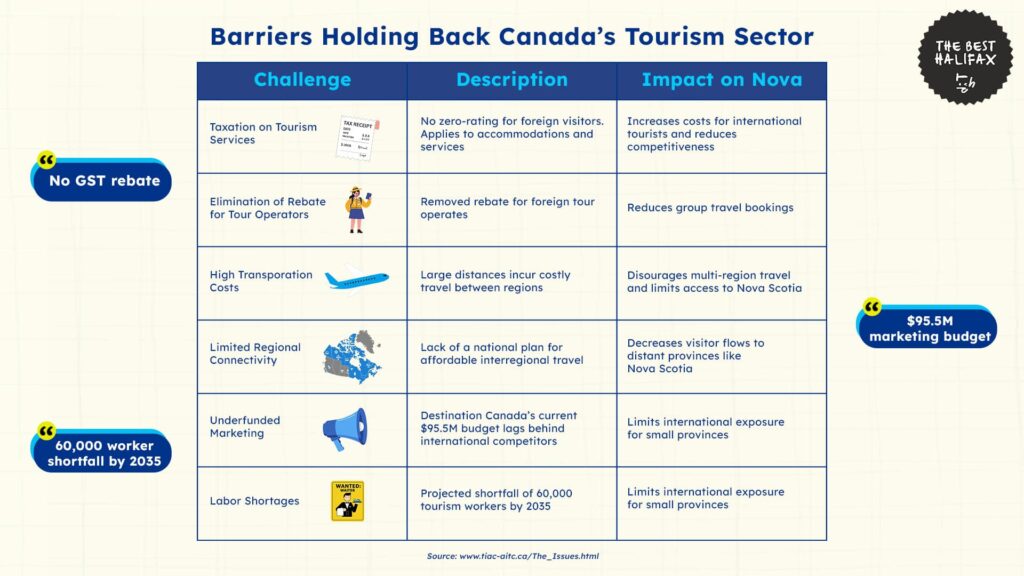

The Tourism Industry Association of Canada shows that while tourism is still an important sector for the economy of Canada, there are policy and structural issues that continue to harm its performance and development.

One of the biggest challenges is that Canada is not tax-competitive in the international tourism economy. The country is one of the few economies that does not zero-rate its tourism services for foreign visitors.

What this does is ensure that international tourists must pay Goods and Services Tax (GST) on accommodation and other travel-related purchases even though, technically, these are export services.

This imposes a direct expense on international travelers in the country and causes Canadian tourist areas to be less competitive.

The elimination of the accommodation rebate for incoming tour operators has also undermined Canada’s standing in the group and incentive travel markets. This lowers international tour sales and discourages travel organizers from marketing Canada.

Aside from tax-related issues, Canada’s huge geographical size places high travel and transportation costs on tourists.

For foreign visitors who want to visit several areas, the price of flights and long-distance transportation usually makes multi-destination travel economically difficult or even impossible.

This disproportionately affects distant areas such as Nova Scotia, whose tourism relies significantly on long-haul visitors from elsewhere in Canada or overseas.

Limited availability of low-cost air travel and the lack of a national plan to enhance regional connectivity limits visitor flows and diminishes economic opportunities for local businesses.

Underinvestment in marketing is another contributing factor to the industry’s inability to expand. Destination Canada has a base annual budget of $95.5 million, far below the marketing expenditure of rival destinations like Australia and Ireland.

This budget restricts Canada’s efforts to effectively brand its tourism within foreign markets. Consequently, smaller provinces like Nova Scotia suffer from a lack of exposure to world travelers, especially against nations with stronger marketing.

Meanwhile, shortages in the labor force remain an issue throughout the tourist industry. With 1.8 million tourism jobs supported in Canada, the industry is a significant employer of youth, newcomers, and Indigenous peoples.

However, workforce shortages are increasing. Tourism HR Canada anticipates that the industry will experience a shortage of 60,000 employees by 2035 if policies do not change.

These shortages lower service capacity, restrict business hours, and have an impact on the quality of the visitor experience.

For places like Nova Scotia that depend on seasonal peaks of tourism, the inability to fully staff hotels, restaurants, and attractions directly impacts the number of visitors that can be accommodated.

All these issues combined diminish competitiveness, decrease return on investment for domestic tourism enterprises, and lower growth in urban and rural areas.

Interventions and Solutions to Weak Tourism Policies

The same report by the Tourism Industry Association of Canada offers options to resolve the financial and structural impediments confronting the tourism industry.

A core solution is the recapture of export status for tourism. The existing taxation system differentiates tourism from the rest of Canadian exports by taxing goods bought by foreign tourists under the Goods and Services Tax.

The reimposition of GST rebates on hotel accommodations for international tour operators could cut the expense of group and package travel, enhancing Canada’s competitiveness in price in the global arena and promoting greater bookings.

Returning the rebate would reverse some of the harm caused by its elimination, which undermined Canada’s footing in the international tour market.

The second major intervention is pumping more federal funding into tourism promotion. With a long-term, stable fiscal model for Destination Canada, it can better compete with other national tourism organizations.

Extra funding would also improve ongoing advertising campaigns and enhance market studies. This would benefit areas like Nova Scotia directly by promoting international awareness and attracting more tourists.

Moreover, expanding access and affordability of air transportation is also a key goal. Canada has some of the world’s highest aviation fees, which makes traveling costs for both domestic and foreign visitors prohibitive.

The federal government can take steps to lower these charges and invest in enhancing aviation infrastructure and connectivity. This would improve access to smaller markets such as Nova Scotia and improve multi-destination travel throughout Canada.

Alongside this, policy shifts that enable tourism employers could more easily attract and retain employees.

This would involve simplifying immigration options for tourism employment, designating tourism as a priority sector in labor policy, and enhancing funding for training and retention initiatives.

By addressing taxation, marketing, access, and labor issues, the federal government can assist in unlocking more economic benefits from tourism and ensure that Nova Scotia becomes more competitive in an increasingly dynamic global travel landscape.

The Future of Tourism in Halifax

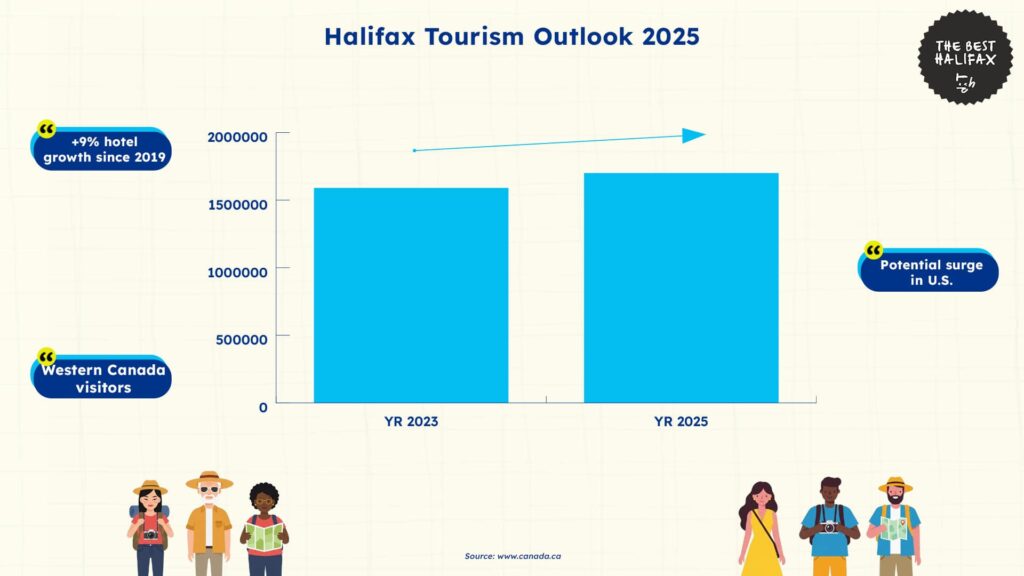

Based on recent trends and recovery patterns, Halifax is set to experience ongoing growth in tourism activity over the next several years.

Hotel nights have already exceeded pre-pandemic levels at 1,588,921 in 2023, an increase of 9% over 2019. Assuming this rate continues, Halifax will potentially surpass 1.7 million hotel room nights sold by 2025.

Room-share bookings, though recovering more slowly, increased to 280,500 stays in 2023. This stable growth implies the sector could hit 300,000 in the next years if the demand for flexible accommodation continues to rise.

Employment is also anticipated to increase, with 34,000 jobs related to tourism already registered in 2019. However, labor gaps and staffing shortages could hinder the sector’s ability to take advantage of these demands.

If federal funding for Destination Canada is increased and airfares are lowered, Halifax might experience more international interest, particularly from long-haul markets like the United States and Western Canada.

Overall, as long as tourism policies are strengthened, Halifax is positioned to become one of the country’s leading tourist destinations.

References

- Discover Halifax. (2020, February). A decade of tourism growth. https://discoverhalifaxdmo.com/media/news/2020/02/a-decade-of-tourism-growth

- Tourism Nova Scotia. (n.d.). Accommodation statistics. https://tourismns.ca/accommodation-statistics

- Halifax Partnership. (n.d.). Halifax Index: Economy – Tourism & Overnight Stays. https://halifaxpartnership.com/research-strategy/halifax-index/economy/#tourism_overnight-stays

- Tourism Nova Scotia. (2024, August). 2022 Visitor exit survey: Visitor profile. https://tourismns.ca/sites/default/files/2024-08/VES22_VisitorProfile.pdf

- Library of Parliament. (2021). Supporting tourism in Canada after COVID-19 (Publication No. 2021-33-E). https://lop.parl.ca/sites/PublicWebsite/default/en_CA/ResearchPublications/202133E?

- Tourism Industry Association of Canada. (n.d.). The issues. https://tiac-aitc.ca/The_Issues.html

- Statistics Canada. (n.d.). Table 23-10-0253-01: Canadian residents returning from the United States or overseas, by type of transportation. https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=2310025301

- Immigration, Refugees and Citizenship Canada. (n.d.). Destination Canada Mobility Forum. Government of Canada. https://www.canada.ca/en/immigration-refugees-citizenship/services/work-canada/hire-temporary-foreign/french-speaking-bilingual-workers-outside-quebec/destination-canada.html

- Tourism HR Canada. (n.d.). Tourism HR Canada. https://tourismhr.ca/